Introduction

Contract workers now make up 7.4% of total U.S. employment, according to Bureau of Labor Statistics data from November 2024. For businesses, that represents a significant talent pool available for project-based, interim, and specialized work.

Tapping that pool isn't as simple as bringing on a freelancer and skipping the paperwork. Many employers stumble on the same issues: misclassifying workers, skipping formal contracts, missing tax filing deadlines, or inadvertently treating contractors like employees — all of which carry real legal and financial consequences.

This guide covers everything you need to hire contract workers correctly — from classification and documentation to the compliance mistakes that cost businesses the most.

Key Takeaways

- A contract employee (independent contractor) is a self-employed professional hired for a specific project or duration — not a W-2 employee on payroll.

- Worker misclassification exposes businesses to back taxes, penalties, and DOL enforcement actions.

- Five steps cover the hiring process: define scope, source candidates, vet, draft a contract, and onboard.

- Key documents: a W-9, a written contractor agreement, and a 1099-NEC for contractors paid $600+ in the calendar year.

- Controlling how a contractor works, not just what they deliver, is the clearest route to a misclassification violation.

What Is a Contract Employee?

A contract employee (more precisely, an independent contractor) is a self-employed professional hired to complete a defined scope of work for a set period. They work under a contract — not as a salaried or hourly employee on your payroll.

The practical differences from a W-2 employee are significant:

- Taxes: Contractors pay their own self-employment taxes (15.3% covering Social Security and Medicare). You don't withhold anything.

- Benefits: No health insurance, PTO, or retirement contributions from the hiring company.

- Compensation: Contractors invoice for their work rather than receiving a regular paycheck.

- Schedule and process: They set their own hours and determine how they achieve the deliverable.

Common Contract Roles by Sector

Those distinctions shape which roles tend to fit the contractor model — particularly in financial services, insurance, and technology:

- Financial analysts and compliance consultants on regulatory projects

- Underwriters covering peak-demand or leave periods

- Technology professionals for system implementations, cloud migrations, or cybersecurity assessments

- Marketing strategists for campaign launches or channel buildouts

- Risk and compliance specialists for audit cycles or M&A integration

- Executive Assistants, Chief of Staff, and HR professionals for interim coverage

The sections below walk through exactly how to structure, source, and onboard these engagements.

Why Businesses Hire Contract Employees

The Cost Case

Employers don't withhold or pay payroll taxes for true independent contractors. There are no benefits to fund, and — depending on the arrangement — no equipment costs. For roles where the workload is cyclical or tied to a specific project, this structure is substantially cheaper than carrying permanent headcount.

Contract staffing is a common solution for:

- M&A integration support and post-deal transitions

- Regulatory compliance projects with defined timelines

- Seasonal demand surges requiring temporary capacity

- Maternity or leave coverage without long-term commitment

Speed and Flexibility

Contract hires move faster than permanent placements. There's no lengthy notice period on either side, no benefits enrollment cycle, and onboarding can be scoped tightly to the project requirements. For businesses that need to respond to a sudden workload spike or fill a gap left by a departing employee, the speed advantage is real.

Ikon Search, for example, typically presents qualified contract candidates within 2-3 days across financial services, insurance, technology, and corporate services — a fraction of the time most internal recruiting teams require for permanent roles.

Expertise on Demand

Contract employees are usually engaged precisely because they bring specialized skills a business needs temporarily. Common examples include:

- A compliance specialist brought in for a new regulatory requirement

- A cloud architect engaged for a platform migration

- A performance marketing lead hired for a product launch

These are time-boxed engagements where a highly skilled contractor delivers more value than a generalist permanent hire.

How to Correctly Classify a Contract Employee

Misclassify a worker and the IRS can hold your business liable for unpaid income tax withholding, Social Security, Medicare, and unemployment taxes — with no reasonable-basis defense available. The financial exposure is real: a January 2024 DOL enforcement action recovered $180,299 in back wages and damages from a single misclassification case involving security guards, plus civil money penalties on top of that.

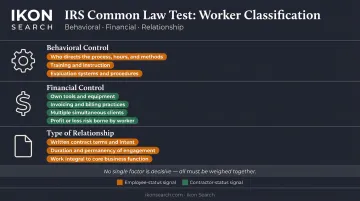

The IRS Three-Factor Common Law Test

The IRS groups classification evidence into three categories. No single factor is decisive; all must be weighed together.

Behavioral Control

Does your company control what the worker does and how they do it? A contractor should direct their own process. Dictating hours, requiring specific methods, and assigning daily tasks all point toward an employment relationship — not a contractor one.

Financial Control

Contractors bear financial risk and independence. Ask whether the worker:

- Uses their own tools and equipment

- Invoices for work (rather than receiving a set salary)

- Works for multiple clients

- Bears the risk of profit or loss on the engagement

All of these point toward contractor status. A worker financially dependent on one company, using that company's equipment and workspace, looks like an employee.

Type of Relationship

Certain contractual and structural facts can override everything else. Flag these as warning signs:

- Written contracts that describe benefits (health insurance, PTO, retirement)

- Indefinite or permanent duration with no defined project end

- Work that is core and ongoing to the business, not a discrete project

These three factors rarely all point the same direction. When they don't, that ambiguity itself is a signal worth taking seriously.

When Classification Is Unclear

If you can't confidently apply these factors, two options exist. First, consult an employment attorney before the engagement starts — especially for complex, ongoing, or high-value arrangements. Second, submit IRS Form SS-8 to request an official determination, though the IRS notes that review may take at least six months.

State-level rules add another layer. California, Massachusetts, and New Jersey all apply stricter ABC tests that presume employee status unless the hiring entity satisfies all three prongs. If you're engaging contractors in these states, the federal IRS test is a floor, not a ceiling.

How to Hire a Contract Employee: Step-by-Step

Step 1: Define the Scope of Work

Before sourcing anyone, document:

- Specific deliverables and success criteria

- Project timeline and engagement duration

- Required skills and experience level

- How the contractor will be compensated (hourly vs. project-based)

This isn't just administrative discipline — a clearly defined scope prevents misclassification, sets contractor expectations, and forms the foundation of your contract agreement.

Step 2: Source and Identify Candidates

Sourcing channels worth considering:

- Industry-specific job boards for sector-relevant talent

- Professional networks (LinkedIn) for passive candidates

- Freelance platforms for generalist or lower-complexity work

- Referrals from trusted colleagues or former contractors

- Specialized staffing firms for time-sensitive or highly technical needs

For specialized needs in financial services, insurance, technology, or corporate services, working with a dedicated contract staffing firm compresses the timeline considerably. This matters most when a compliance project or system implementation has a firm start date. Ikon Search's contract division, led by Kristin Lutz, typically presents qualified candidates within 2-3 days across these verticals.

Step 3: Evaluate and Vet Candidates

Assess contract candidates differently than permanent hires:

- Review a portfolio or work samples relevant to your deliverable

- Conduct structured interviews focused on outcomes, not just responsibilities

- Check references specifically from previous contract engagements

- Administer a technical assessment where the role demands it

- Verify their track record of completing similar engagements on schedule

The key question is simple: can this person operate independently and deliver? Team hierarchy fit matters far less than demonstrated output.

Step 4: Draft and Sign a Contract Agreement

Once you've selected a candidate, formalizing the engagement in writing protects both sides. Every contractor agreement should include:

| Element | What to Cover |

|---|---|

| Scope of work | Specific deliverables, not just a job description |

| Compensation | Rate, payment schedule, invoicing process |

| Timeline | Start date, milestones, end date or review point |

| IP and confidentiality | Who owns the work product; what stays confidential |

| Termination provisions | Notice periods, grounds for early termination |

| Contractor status | Explicit language confirming the independent contractor relationship |

A well-drafted contract is both a legal protection and a classification safeguard. Verbal agreements or loosely worded scopes create disputes over payment and IP that are difficult and expensive to resolve.

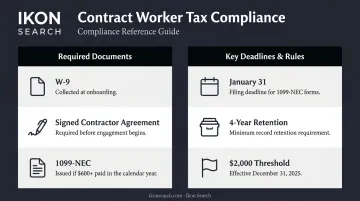

Step 5: Complete Onboarding Documentation

With the contract signed, the final step before work begins is documentation. Collect:

- Signed W-9 (or W-8BEN for foreign contractors) — retained by you, not filed with the IRS

- Finalized contract — signed by both parties

- Access and tools the contractor needs to start

Set expectations around communication cadence and deliverable review — but don't direct when or exactly how the work is performed. That's the line between managing a contractor relationship and creating an employee relationship.

Legal Compliance, Documentation, and Common Pitfalls

Core Tax Obligations

If a contractor earns $600 or more in a calendar year, you must file Form 1099-NEC with the IRS and deliver a copy to the contractor by January 31 of the following year. The W-9 you collected at onboarding provides the taxpayer identification information you need to complete this filing. Retain all employment tax records for at least four years after the tax becomes due or is paid.

Note: The IRS has indicated the reporting threshold will increase to $2,000 for payments made after December 31, 2025.

Co-Employment Risk

When a contractor is engaged through a staffing agency, both the agency and the client company can carry legal responsibilities to that worker. Co-employment violations arise when the client exercises too much control. That means dictating exact hours, pulling contractors into your performance review system, or supplying all equipment and workspace as if they were on permanent staff.

Misclassification: Behavioral Warning Signs

Specific behaviors that trigger misclassification risk:

- Setting mandatory daily start and end times

- Prohibiting the contractor from working for other clients

- Conducting formal performance reviews under your HR system

- Providing all tools, equipment, and dedicated office space

- Including the contractor in company-wide communications and benefits programs

The IRS isn't bound by what your contract says. If the economic reality of the relationship looks like employment, classification risk exists regardless of what the agreement calls the worker.

Weak or Missing Written Contracts

A verbal agreement or loosely defined scope creates three concrete problems:

- Disputes over what was actually agreed to

- Ambiguity over who owns the work product

- Reduced protection during a misclassification audit

At minimum, the contract should define scope, deliverables, payment terms, IP ownership, and termination conditions before work begins.

Frequently Asked Questions

What is the difference between a contract employee and a full-time employee?

Contract employees are self-employed, invoice for their work, pay their own taxes, and receive no employer-provided benefits. Full-time employees are on payroll with taxes withheld by the employer and typically receive benefits like health insurance and paid time off.

How do I correctly determine if someone qualifies as an independent contractor?

Apply the IRS three-factor common law test: behavioral control, financial control, and type of relationship. The core question is how much control your company has over how the work is performed — not just the final output.

What paperwork is required when hiring a contract employee?

You need a signed contractor agreement, a completed W-9 (or W-8BEN for foreign workers), and a 1099-NEC filed with the IRS if the contractor earns $600 or more in the calendar year.

Do employers pay taxes for contract employees?

No. Employers don't withhold or pay income tax, Social Security, or Medicare taxes for independent contractors — the contractor handles their own self-employment taxes. You are still required to file a 1099-NEC if payments reach the $600 threshold.

What should be included in a contract employee agreement?

At minimum: defined scope of work and deliverables, payment terms and schedule, project timeline, IP ownership and confidentiality clauses, termination conditions, and language confirming the independent contractor relationship.

Can a contract employee transition to a permanent full-time role?

Yes. This is called a temp-to-hire or contract-to-perm arrangement. The transition requires formal reclassification under IRS and DOL guidelines, updated documentation, payroll and benefits setup, and written notification to the worker.