Hiring a bookkeeper is less about offloading paperwork and more about protecting your business's financial clarity. This guide covers exactly what a bookkeeper does, the five signs you need one now, which hiring model fits your situation, and the step-by-step process to find the right person with confidence.

Key Takeaways

- Bookkeepers handle daily recordkeeping; accountants handle strategy, tax filing, and audits — most businesses need both

- Most small businesses don't need a full-time hire—part-time, freelance, or virtual arrangements work well

- Nearly 4 in 10 U.S. small business owners manage finances on their own, often sacrificing accuracy and growth focus

- Credentials like NACPB, AIPB, and QuickBooks ProAdvisor signal competence but aren't legally required

- A written contract with defined scope, pricing, and data access terms is non-negotiable

What Does a Bookkeeper Actually Do?

The simplest way to frame it: bookkeepers keep your financial records accurate and current. Accountants interpret and act on those records.

According to the Bureau of Labor Statistics, bookkeeping clerks compute, classify, and record numerical data to keep financial records complete—performing routine calculating, posting, and verification work. Accountants, by contrast, prepare and examine financial records, identify risks, and provide business solutions.

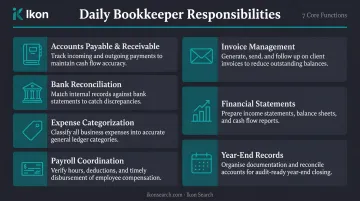

What a Bookkeeper Handles Day-to-Day

- Tracks accounts payable and receivable so you always know what you owe and what's owed to you

- Reconciles bank statements against your records on a monthly basis

- Categorizes expenses correctly to keep transactions tax-ready

- Coordinates payroll with providers or processes it directly

- Issues, tracks, and follows up on client invoices

- Produces profit and loss statements, balance sheets, and cash flow summaries

- Organizes year-end records for your CPA or tax preparer

That scope has clear limits, though. A bookkeeper does not file your taxes, provide strategic financial advice, conduct audits, or represent you before the IRS. Those functions require a CPA or enrolled agent.

Most small and mid-sized businesses don't need a full-time in-house bookkeeper. Part-time or contract arrangements handle the workload adequately—and at a fraction of the cost.

Signs Your Business Needs a Bookkeeper Now

You're Spending Hours on Data Entry Each Week

When you're logging transactions instead of closing deals or managing operations, bookkeeping is consuming time that should go toward growth. Half of U.S. small businesses encounter fiscal challenges due to a lack of financial literacy, and 39% are handling financial matters entirely on their own. That independence often comes with a hidden cost: decisions built on incomplete or inaccurate data.

Your Books Are Behind or Unreliable

Stale records make it impossible to know where your business actually stands. You can't manage cash flow you can't see. 45% of small businesses report cash flow problems, and 60% wait more than 30 days for invoice payments—issues that become far more painful when your books aren't current enough to flag them early.

Tax Season Feels Like a Crisis

If every January or April involves scrambling through folders, chasing receipts, and holding up your accountant with missing records, that's a process problem, not a paperwork problem. A bookkeeper maintains audit-ready records throughout the year, which means tax prep becomes a handoff, not a marathon.

You're Scaling or Adding Financial Complexity

Hiring employees, adding revenue streams, or pursuing financing all increase recordkeeping demands fast. Key requirements at this stage include:

- Timely, accurate financial statements for SBA loan applications, including accounts receivable and payable aging reports

- Clean books that banks and investors require before committing capital

- Organized records ready at the moment a deal moves forward — disorganized financials can kill it

You've Missed Payments or Lost Track of Cash

The numbers here are unforgiving. The IRS Failure to Deposit Penalty for employment taxes starts at 2% for deposits 1–5 days late and reaches 15% once the IRS issues a formal notice. At the same time, 56% of small businesses are owed money from unpaid invoices, averaging $17,500 per business. Both are direct, measurable costs of recordkeeping that slips.

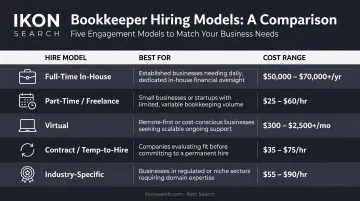

Types of Bookkeepers: Which Model Fits Your Business?

| Hire Model | Best For | Cost Range |

|---|---|---|

| Full-time in-house | High-volume businesses needing daily financial management | Salary + benefits ($49K+ annually per BLS) |

| Part-time or freelance | Small businesses with periodic reconciliation needs | $11–$40+/hour depending on complexity |

| Virtual bookkeeper | Businesses comfortable with cloud accounting tools | $100–$600+/month via service firms |

| Contract or temp-to-hire | Businesses needing immediate help with flexibility to assess fit | Varies; staffing firm-facilitated |

| Industry-specific bookkeeper | Businesses in real estate, financial services, e-commerce, healthcare | Premium over generalist rates |

A Closer Look at Each Model

Part-time and freelance works for most small businesses with periodic reconciliation needs. The QuickBooks ProAdvisor directory and Xero Advisor directory both list credentialed professionals by location and specialty.

Virtual bookkeepers deliver the same core services as in-house staff at lower overhead. Platforms like Bench and Pilot offer tiered monthly plans with pricing that adjusts as your business grows.

Contract or temp-to-hire makes sense when you need help quickly but aren't ready for a permanent commitment — common in financial services, where bookkeeping often needs to integrate with broader finance teams. Staffing firms like Ikon Search, which places contract and full-time accounting and finance professionals across financial services, technology, and insurance, can typically present a qualified shortlist within two to three days.

Industry-specific bookkeepers are worth the premium when your business has niche compliance or reporting requirements — think fund accounting for a hedge fund or percentage-of-completion for a construction firm. The reduced onboarding time alone often offsets the higher rate.

How to Hire a Bookkeeper: A Step-by-Step Process

Step 1 — Define Your Needs Before You Search

Before posting anywhere, answer these questions:

- How many transactions does your business process monthly?

- Do you need basic data entry and reconciliation, or payroll support, financial reporting, and multi-entity accounting?

- Full-time, part-time, or contract?

- What's your realistic monthly budget?

Clear answers here keep your search focused and your candidate pool relevant from the start.

Step 2 — Source Candidates Through the Right Channels

Your options:

- Referrals from your accountant, attorney, or trusted peers (often the fastest path to a reliable hire)

- Professional directories — QuickBooks ProAdvisor and Xero Advisor filter by certification and location

- Freelance platforms — Upwork and LinkedIn for independent bookkeepers

- Job boards — Indeed or LinkedIn for part-time or full-time roles

- Staffing firms — firms like Ikon Search, which runs a dedicated Corporate Services practice covering accounting and finance support, can deliver a vetted shortlist in 2–3 days for businesses that need qualified candidates without a lengthy search

Step 3 — Screen for Credentials and Relevant Experience

Look for:

- NACPB Certified Public Bookkeeper (CPB) or AIPB Certified Bookkeeper designation

- QuickBooks ProAdvisor certification if your business uses QuickBooks

- Demonstrated experience with businesses of similar size and industry

- Verifiable references from prior clients—ask specifically about accuracy, communication, and how they handle errors

Certifications are not legally required, but they signal that a candidate has been tested on real bookkeeping competencies, not just self-taught habits.

Step 4 — Conduct a Structured Interview

Go beyond résumé review. Key questions to ask:

- What types of businesses do you typically work with, and how is mine similar or different?

- Walk me through your month-end close process.

- How do you catch and correct errors—can you give me a specific example?

- How and how often do you communicate with clients?

- Are you available and fully operational during tax season and year-end?

The interview also tells you about communication style. A technically sharp bookkeeper who's difficult to reach or vague about their process is a risk.

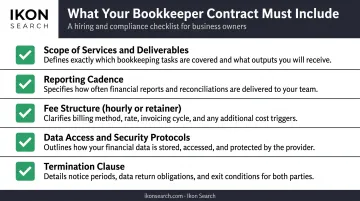

Step 5 — Formalize with a Written Contract

Once you've selected a candidate, put everything in writing:

- Scope of services and specific deliverables

- Reporting cadence (weekly, monthly)

- Fee structure—hourly or flat monthly retainer

- Data access and security protocols

- Clear termination clause

A written agreement protects both parties and removes the ambiguity that leads to scope creep or missed deliverables.

What to Look for in a Bookkeeper

Credentials Worth Prioritizing

- NACPB CPB — requires accounting education, a three-part exam, one year of experience under a CPA or CPB, and adherence to a professional code of conduct

- AIPB Certified Bookkeeper — covers adjusting entries, payroll, depreciation, inventory, and internal controls

- QuickBooks ProAdvisor — requires annual recertification, covers QuickBooks Online, Desktop, and Enterprise

- Software proficiency — Xero, FreshBooks, or whatever platform your business uses

Credentials confirm competence. Soft skills determine whether the working relationship actually holds up.

Soft Skills That Matter as Much as Technical Ability

- Attention to detail—errors in bookkeeping compound quickly

- Discretion with sensitive financial data

- Proactive communication when something looks wrong

- Organizational consistency, especially around month-end deadlines

Trustworthiness is non-negotiable. A bookkeeper has access to your bank accounts, payroll data, and full financial history. References exist to validate this.

Red Flags to Watch During the Hiring Process

- Can't walk you through their process or name past software—a qualified bookkeeper answers both without hesitation. Evasiveness on either is disqualifying.

- Avoids putting scope, pricing, and responsibilities in writing—this creates the conditions for disputes and gaps in accountability. Require a formal contract before moving forward.

Frequently Asked Questions

How much does a bookkeeper cost?

Freelance bookkeepers on platforms like Upwork typically charge $11–$40+ per hour depending on complexity and experience. Virtual bookkeeping services often run $200–$600/month for small businesses, with pricing scaling based on transaction volume and service scope. In-house employees average $49,210/year in median wages per BLS data.

What's the difference between a bookkeeper and an accountant?

Bookkeepers maintain daily financial records—recording, categorizing, and reconciling transactions. Accountants handle higher-level work: tax filing, financial forecasting, audits, and strategic advice. CPAs hold state-board-governed licenses; bookkeepers do not require equivalent licensing.

Should I hire full-time, part-time, or freelance?

Match the model to your transaction volume. Most small businesses do fine with part-time or freelance support—it keeps costs in line with actual workload. Full-time, in-house bookkeepers make sense when daily financial activity requires constant hands-on management.

What certifications should a bookkeeper have?

Look for NACPB Certified Public Bookkeeper (CPB), AIPB Certified Bookkeeper, or QuickBooks ProAdvisor status. These are private professional credentials, not government licenses—but they indicate tested competence and accountability.

What questions should I ask when interviewing a bookkeeper?

Focus on these four questions to assess both competence and reliability:

- What businesses similar to mine have you worked with?

- How do you handle your month-end close?

- How do you catch errors—can you give an example?

- How available are you during tax season?